A DSA, or Direct Selling Agent, is an entity authorized by a bank or NBFC to source and refer loan applicants. A DSA doesn’t lend money itself. If you’ve used a loan comparison platform before, a DSA-style model was likely involved somewhere in the process.

This guide explains what a DSA does, how the model works, and how TapTapLoans fits into it.

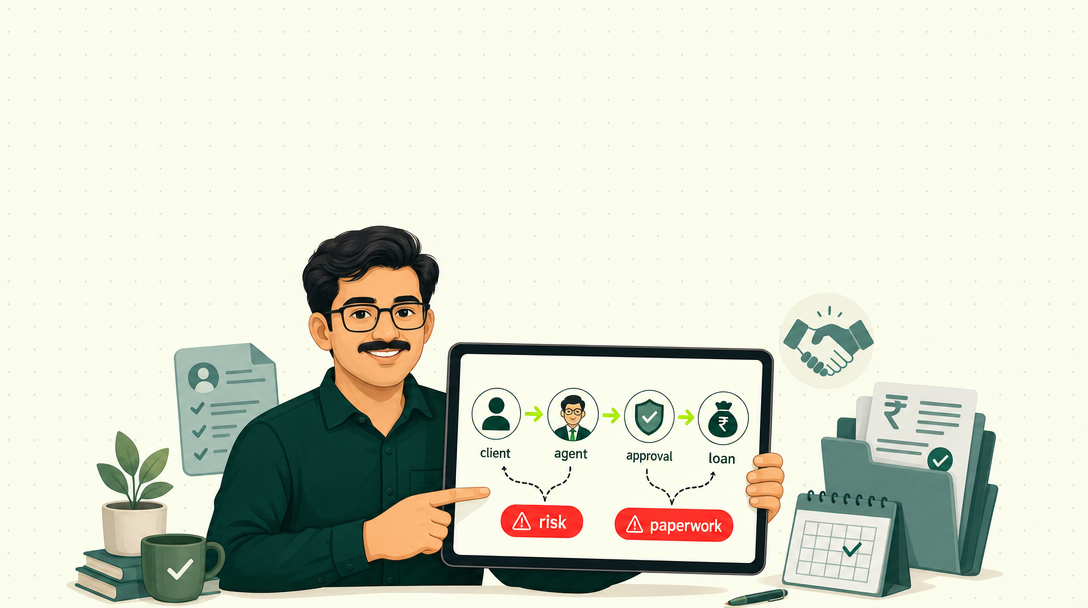

What a DSA Actually Does

A DSA acts as a bridge between borrowers and lenders. Instead of visiting five banks individually, a DSA can check your eligibility across multiple lenders at once. It then refers you to the ones most likely to approve you.

The DSA doesn’t underwrite the loan. It doesn’t disburse funds. It doesn’t hold your deposits. The lending decision, and the money itself, comes entirely from the regulated bank or NBFC.

How DSAs Are Regulated

Banks and NBFCs must have proper agreements with any DSA they work with. DSAs are expected to follow RBI’s fair practices code. This means accurate representation of rates and fees, no misleading claims, and clear disclosure of who the actual lender is.

A legitimate DSA is always transparent about which banks or NBFCs’ personal loans it partners with, by name.

How the DSA Model Benefits Borrowers

Applying to multiple banks individually means multiple hard credit inquiries. Each one can dent your CIBIL score for personal loans. It also means repeated paperwork, over and over.

A DSA-style platform checks your eligibility across many lenders with a single soft inquiry. This doesn’t affect your score. You see your real options before committing to a full application with any one lender.

How TapTapLoans’ Advisory Model Works

TapTapLoans operates on this same principle. Here’s the process, step by step.

- You share your requirements. Loan amount, purpose, and basic profile details.

- We check your eligibility across our lender network. This uses a soft credit check, with no impact on your score.

- You see your real options, with transparent rate and fee information for each.

- You choose a lender. Your application proceeds directly with that regulated bank or NBFC.

- The loan is disbursed by the lender, not by TapTapLoans.

We don’t lend money ourselves. Every loan comes from a licensed, RBI-regulated partner.

How TapTapLoans Is Compensated

[State the actual model clearly here. Commonly, DSA-style platforms are compensated by the lender upon successful disbursement, not by the borrower directly. Confirm and publish your specific structure.]

DSA vs Direct Bank Application: What’s the Real Difference?

| Factor | Applying Directly to One Bank | Going Through a DSA-Style Platform |

|---|---|---|

| Applications | One at a time | Multiple lenders checked at once |

| Credit score impact | One hard inquiry per bank | One soft inquiry, then one hard inquiry with your chosen lender |

| Rate comparison | Manual, one offer at a time | Multiple offers shown together |

| Who actually lends | The bank | Always the bank or NBFC, never the DSA itself |

Questions to Ask Any DSA-Style Platform Before Applying

Which specific banks or NBFCs do you work with? A legitimate platform names them clearly. Does checking my eligibility involve a soft or hard credit inquiry? Are there fees charged to me directly, or is compensation only from the lender? Who is the actual lender once I’m matched, and can I verify their RBI registration?

If a platform can’t answer these clearly, treat that as a caution sign.

Why This Model Matters for Borrowers With Complex Profiles

Self-employed applicants, borrowers with a shorter credit history, or those already rejected by one bank, often benefit the most from this model. A rejection from one lender doesn’t mean you’re ineligible everywhere. Different lenders have different risk appetites.

Checking multiple options at once, rather than one rejection at a time, saves both time and unnecessary hits to your credit score.

A Common Misunderstanding About DSAs

Some borrowers assume a DSA is somehow a “middleman” adding extra cost to their loan. In a properly disclosed model, this isn’t accurate. The lender pays the DSA for referring a qualified applicant; the same cost structure exists whether you find that lender yourself or through a DSA. What you gain through a DSA-style platform is the ability to compare multiple lenders at once, not an added cost.

Frequently Asked Questions About DSAs and Loan Advisory Platforms

No. A DSA refers and assists borrower applications to banks and NBFCs, but doesn’t lend money itself. The actual loan comes from the regulated institution.

This varies by platform. Many DSA-style platforms are compensated by the lender upon successful disbursement, not the borrower. Always confirm the specific fee structure of any platform you use.

Checking your eligibility typically uses a soft inquiry, which doesn’t affect your score. A hard inquiry only occurs once you proceed with a specific lender’s full application.

Check that they clearly name their partner banks and NBFCs, and that those lenders are RBI-regulated. A legitimate DSA is transparent about this, not vague.

TapTapLoans operates on a DSA-style advisory model, connecting borrowers with our RBI-regulated bank and NBFC partners. We don’t lend money directly ourselves.

Want to see which lenders you qualify with? Check your eligibility with TapTap, a soft credit check across 20+ lenders, with zero impact on your score.