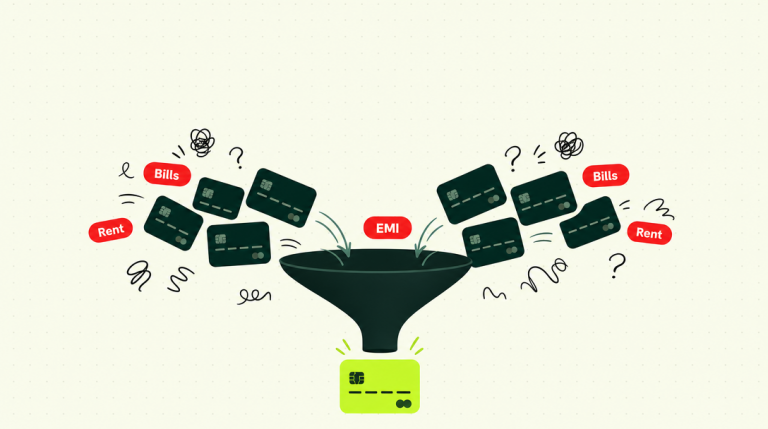

If you’re managing three or four EMIs every month — a personal loan here, a credit card bill there, maybe a consumer finance EMI on top — you already know the problem. It’s not just the money. It’s the mental overhead of keeping track of due dates, lenders, and balances. One missed payment and your CIBIL score takes a hit you’ll spend months fixing.

Loan consolidation is a way to simplify all of that. It doesn’t erase your debt, but it reorganizes it — ideally at a lower interest rate and with a single monthly payment instead of several. This guide covers how it works in India, who should do it, and what the actual numbers look like.

What is Loan Consolidation?

Loan consolidation means taking a new loan — typically a personal loan — to pay off all your existing debts at once. After that, you owe money to just one lender, make one monthly payment, and ideally pay a lower interest rate than what you were averaging across your old debts.

The term is sometimes used interchangeably with “debt consolidation,” and in the Indian lending context, both refer to the same mechanism: a single personal loan that clears multiple outstanding balances. The key difference from a balance transfer is scope — a balance transfer moves one specific loan to a new lender, while loan consolidation combines several debts into one.

How Loan Consolidation Works in India

The process is more straightforward than most borrowers expect:

- Calculate your total outstanding debt — list every loan, its outstanding principal, interest rate, and remaining tenure.

- Apply for a personal loan — request an amount equal to or greater than your total outstanding balance across all debts.

- Use the disbursed amount to close existing loans — some lenders disburse directly to the creditors; others credit your bank account.

- Begin single-EMI repayment — you now owe one lender, pay one EMI, on one due date.

In India, banks and NBFCs typically process loan consolidation applications within 2–5 working days. Digital-first lenders and loan advisory platforms can cut that to 24–48 hours for pre-approved borrowers.

Who Should Consider Loan Consolidation?

Not every borrower benefits from loan consolidation . It makes sense when at least two of the following conditions are true:

- You are managing three or more active loan EMIs simultaneously.

- At least one of your existing loans carries an interest rate above 18% — particularly credit card debt, which averages 36–42% per annum in India.

- Your CIBIL score has improved since you took your original loans, making you eligible for a lower rate today.

- You’re missing or at risk of missing EMI due dates because of the volume of payments.

- Your take-home salary or business income has grown, improving your FOIR (Fixed Obligation to Income Ratio).

If your existing loans are at rates below 12%, and you’re managing payments without difficulty, loan consolidation may not save you enough to justify the processing fees and paperwork.

Types of Debts You Can Consolidate

In India, the following debt types are eligible for loan consolidation via a personal loan:

- Existing personal loans from banks or NBFCs

- Credit card outstanding balances (revolving or EMI)

- Consumer durable loans (electronics, appliances)

- Education loans (in some cases)

- Two-wheeler or vehicle loans (subject to lender policy)

Home loans and secured loans are generally not consolidated through this route — they require a separate balance transfer product.

What Does Loan Consolidation Cost?

This is where many borrowers underestimate the full picture. Before doing loan consolidation , account for:

The break-even point — where your interest savings exceed the total cost of consolidation — typically falls between 9 and 18 months. If you plan to close the new loan before that, the exercise may not be worth it financially.

Loan Consolidation Eligibility in India

Standard eligibility criteria for a loan consolidation personal loan in 2026:

- Age: 21 to 60 years (at loan maturity)

- CIBIL Score: 700+ for competitive rates; some NBFCs approve at 650+

- Employment: Salaried (minimum 1 year with current employer) or self-employed with 2+ years of ITR

- Minimum net monthly income: ₹20,000 (varies by city and lender)

- FOIR: Total EMIs (including new loan) should not exceed 50–55% of net monthly income

Risks and Limitations of Loan Consolidation

Three risks worth understanding before you proceed:

Longer tenure = more total interest paid. If you consolidate ₹5 lakh across 5 years instead of 2 years, you may pay less monthly, but you pay interest for longer. Run the total interest calculation, not just the EMI comparison.

No discipline benefit without habit change. Loan consolidation clears your credit card balance — but if you continue spending on those cards, you’ll end up with the new loan EMI plus fresh card dues. The math works against you fast.

Hard inquiry on CIBIL. Applying for the consolidation loan triggers a hard inquiry, which can temporarily lower your score by 5–10 points. This recovers within 3–6 months of consistent repayment.

- Loan consolidation combines multiple debts into a single personal loan with one EMI and ideally a lower interest rate.

- It works best when you have high-interest debt (especially credit cards at 36–42% p.a.) and a CIBIL score above 700.

- Always calculate the break-even point before proceeding — account for processing fees and foreclosure charges.

- FOIR must stay under 50–55% of net monthly income for the new consolidated loan to be approved.

- Without a change in spending behavior, consolidation only delays debt — it doesn’t resolve it.

Frequently Asked Questions

Most banks require a CIBIL score of 700 or above for the best rates. Some NBFCs approve loan consolidation applications at 650+, but the interest rate offered will be higher, which may reduce the financial benefit of consolidating.

Yes. A personal loan for debt consolidation can cover both credit card outstanding amounts and existing personal loans simultaneously. The combined outstanding amount becomes the loan principal you apply for.

Most banks and NBFCs process loan consolidation within 2–5 working days after document submission. Digital lenders with pre-approved offers can disburse within 24 hours.

There’s a temporary dip of 5–10 points from the hard inquiry when you apply. However, consistently paying the new single EMI typically improves your CIBIL score over 3–6 months as your credit utilization ratio drops and your repayment history strengthens.

The limit is your eligible personal loan amount, which is determined by your income, CIBIL score, and existing FOIR. Most lenders in India offer personal loans up to ₹40 lakh for loan consolidation purposes.

Conclusion

Loan consolidation is a practical financial tool — not a debt escape hatch. When the numbers work (and they do, for many borrowers with credit card debt and multiple EMIs), consolidating into a single personal loan can cut your interest burden meaningfully and simplify your financial life. The decision should start with your current interest rates, your CIBIL score, and a realistic break-even calculation. If you need help modeling that, a loan advisory platform can do it without triggering any credit inquiry.