Indian weddings cost more than they should. Family pressure, social comparison, and the cultural weight of “it happens only once” push couples and their families into borrowing amounts they wouldn’t borrow for any other reason. The average urban Indian wedding in 2026 costs ₹8–25 lakh. A growing share of that is funded by personal loans, often called “wedding loans” or “marriage loans” in marketing.

Banks love wedding loans because they’re large-ticket and emotionally driven. The borrower rarely runs the long-term math. This blog runs the math you should see before signing: what ₹10 lakh borrowed at 12% actually costs over 10 years, the 4 smarter alternatives that fund weddings without crushing repayment burden, and the mistakes that turn one celebration into a decade of debt.

The Indian Wedding Loan Landscape (2026)

Most “wedding loans” are simply personal loans marketed as such. The loan itself has no special structure; the marketing positions it for the use case. Common features:

- Loan amount: ₹1L–40L typically; some lenders go up to ₹75L.

- Interest rate: 11–20% depending on CIBIL and income.

- Tenure: 12–60 months.

- Documents: Same as standard personal loan.

- No specific verification of wedding-related use — the lender doesn’t care what you actually spend on.

Lenders and Rates for Wedding Loans

| Lender | Wedding Loan Rate | Maximum Amount | Processing Fee |

|---|---|---|---|

| HDFC Bank | 10.75–16% | ₹40L | 1–2.5% |

| ICICI Bank | 10.85–16.5% | ₹40L | 1–2.5% |

| SBI | 11–14.5% | ₹20L | 1% |

| Axis Bank | 10.99–18% | ₹40L | 1–2% |

| Bajaj Finance | 12–20% | ₹40L | 2–3% |

| Tata Capital | 11–18% | ₹35L | 1–2.5% |

₹10L Wedding Loan: EMI by Tenure

| Tenure | Monthly EMI @ 12% | Total Interest | Total Repayment |

|---|---|---|---|

| 3 years | ₹33,213 | ₹1,95,668 | ₹11,95,668 |

| 5 years | ₹22,244 | ₹3,34,667 | ₹13,34,667 |

| 7 years | ₹17,653 | ₹4,82,852 | ₹14,82,852 |

| 10 years | ₹14,347 | ₹7,21,651 | ₹17,21,651 |

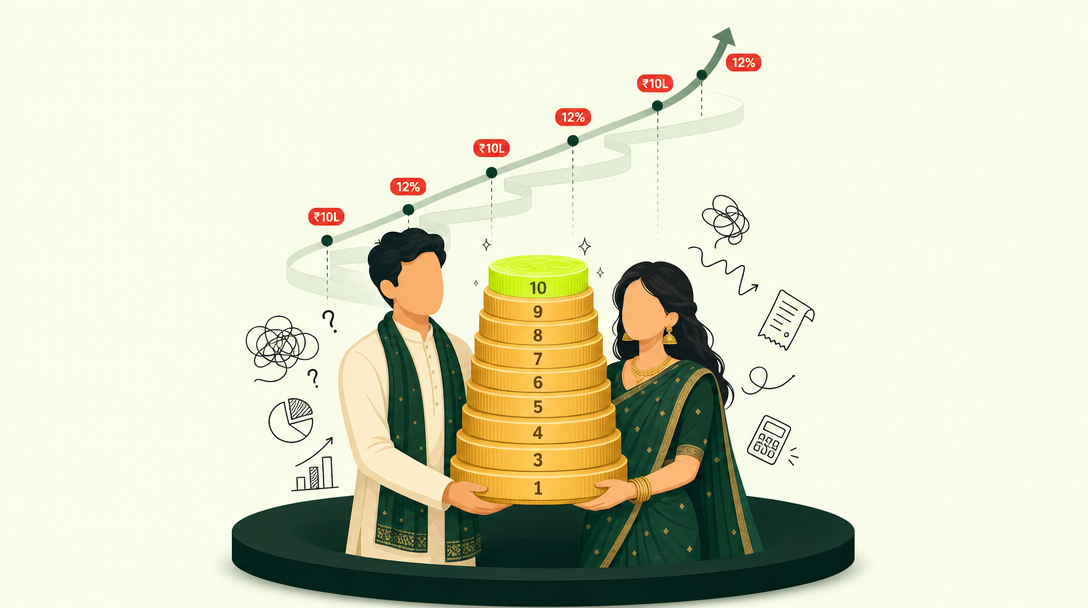

A 10-year tenure has the lowest EMI but the highest total cost. Most borrowers don’t think about the cumulative interest — they look at “can I afford the monthly EMI?” and stop there.

The Real Long-Term Cost

Beyond the interest paid, there’s an even higher cost: opportunity cost.

Scenario:

- Wedding loan of ₹10L at 12% over 5 years.

- EMI: ₹22,244/month.

- Total cash out over 5 years: ₹13,34,667.

- Hypothetical alternative: Same ₹22,244/month invested in a mutual fund SIP earning 12% CAGR.

- Value after 5 years: approximately ₹18.5L.

- Net difference: ₹18.5L investment vs ₹13.35L spent on loan repayment = ₹31.85L spread over the borrower’s first 5 years of marriage.

This is the financial cost of the wedding decision spread across the couple’s early married life. A ₹10L wedding loan effectively costs them a ₹25–35L early-investment opportunity.

4 Smarter Alternatives to a Wedding Loan

Alternative 1: Split Loan + Savings

Borrow only the portion you genuinely cannot pre-fund from savings. If the wedding budget is ₹10L and you have ₹6L in liquid savings, borrow ₹4L instead of ₹10L. EMI drops from ₹22,244 to ₹8,898 over 5 years. Total interest paid drops from ₹3.34L to ₹1.34L.

Alternative 2: Loan Against Gold or FD

If the family has gold or FDs that aren’t needed in the next 2–3 years, a loan against these assets costs 9–11% vs 12–16% for a personal loan. On a ₹10L, 5-year borrowing, this saves ₹1L–1.5L in interest.

See our guides on loan against FD and the use of gold loans for personal loan vs gold loan comparison.

Alternative 3: Family Loan with Clear Repayment Terms

Borrowing from family at 0% (or a token nominal rate) is often the cheapest option. The discipline: treat it like a real loan. Document the terms, repay monthly, don’t let casual goodwill turn into long-term family friction.

Alternative 4: Smaller-Scale Wedding

The least talked-about option: scale the wedding to your means. A ₹5L wedding, well-planned, is more enjoyable than a ₹10L wedding under debt stress. Most guests don’t remember the venue’s chandeliers; they remember the warmth of the hosts.

Mistakes to Avoid

- Mistake 1: Borrowing the maximum the lender approves. Approval limit is the lender’s risk appetite, not your spending limit.

- Mistake 2: Long tenure for lower EMI. Stretching to 7–10 years more than doubles the total interest paid.

- Mistake 3: Multiple loans from multiple lenders. FOIR explodes; you become unable to take other loans during early marriage when home loans matter.

- Mistake 4: Both spouses signing as joint borrowers. If the marriage faces issues later, joint liability complicates matters.

- Mistake 5: Not budgeting for post-wedding life. Honeymoon, home setup, first month’s salary delays — these all happen WHILE your wedding EMI starts.

- Mistake 6: Credit card EMI for venue/catering. Card EMIs at 14–18% beat personal loans only for very short tenures.

How to Repay Fast After the Wedding

If you’ve taken the loan and want to clear it fast:

- Use all wedding cash gifts (shagun, neg) for partial prepayment in the first 30 days.

- Set a 3-year repayment target even if the loan tenure is 5 years — partial prepayments after 12 months.

- Avoid the trap of using your honeymoon/festival money for celebrations while loan EMI accumulates.

- Consider a balance transfer if your rate is high and you can get below 11.5% post-marriage.

- Treat your annual bonus as 100% prepayment, not a lifestyle upgrade.

Frequently Asked Questions

No. Personal loans, including those marketed as wedding loans, are not tax-deductible.

Yes, joint applications can increase loan eligibility. But understand the joint liability — both CIBILs are affected by any default.

Up to 60 months at most lenders; some go up to 84 months. Longer tenure means lower EMI but much higher total interest.

Yes, typically 1–3 percentage points cheaper. If you have gold that won’t be used during the loan tenure, a loan against gold is the better option.

Maintain CIBIL above 750, choose a 3–5 year tenure, compare 3–4 lenders, negotiate the processing fee, and decline bundled insurance.

Q

Bottom Line

A wedding loan is just a personal loan with romantic marketing. The math doesn’t change because of the occasion. Borrow less, repay faster, and never let a one-day event define a decade of finances.

Plan your wedding by borrowing smartly. TapTap Loans helps you find the right loan size and structure, so you’re not paying for the wedding 10 years later.