A joint personal loan involves two borrowers — a primary applicant and a co-borrower — who are both legally responsible for repayment. The primary motivation for most borrowers applying jointly is improved loan eligibility: combining two incomes raises the FOIR headroom, and a stronger co-borrower can compensate for a weaker primary applicant’s credit profile.

But joint personal loans also carry risks that most borrowers understand only after they have signed. Both applicants are equally liable. A default by either party damages both CIBIL scores. This guide explains when a joint application is the right strategic move and when it creates more risk than benefit.

Who Can Be a Co-Borrower in a Joint Personal Loan?

| Relationship | Accepted By | Notes |

|---|---|---|

| Spouse | Most banks and NBFCs | Most common co-borrower relationship; combined income considered |

| Parents | Many lenders | Age of co-borrower matters — must be below retirement age |

| Children (adult) | Some lenders | Co-borrower must be employed with verifiable income |

| Siblings | Select NBFCs | Less commonly accepted; depends on lender policy |

| Business partners | Rare for personal loans | More common for business loans |

Benefits of a Joint Personal Loan

1. Higher Loan Amount

When you apply jointly, both incomes are combined. A couple where each partner earns Rs. 40,000/month may individually qualify for a Rs. 5-8 lakh personal loan. Together, their combined Rs. 80,000/month income could qualify them for Rs. 12-16 lakh — significantly higher than either could access individually.

2. Better Interest Rate if Primary Applicant Has Low CIBIL Score

If the primary applicant has a CIBIL score of 680 (borderline) and the co-borrower has a score of 760 (strong), lenders often use the stronger score or weight both scores in their assessment. This can result in approval at a rate that the primary applicant could not have obtained alone.

3. Improved Approval Probability for Complex Profiles

Borrowers with short employment history, income from non-standard sources, or profiles that individually fall just below a lender’s threshold often succeed with a joint application where the co-borrower’s profile provides the necessary creditworthiness.

4. Both Applicants Build Credit History

A joint personal loan is reported on both applicants’ CIBIL reports. Consistent on-time repayment builds positive payment history for both borrowers simultaneously — a particularly valuable outcome for borrowers with thin credit files.

Risks and Responsibilities Both Borrowers Must Understand

| Both borrowers are 100% responsible for the full loan amount. There is no 50-50 split. If the primary applicant defaults, the lender will pursue the co-borrower for the full outstanding amount — and both CIBIL scores will suffer equally. |

Full liability for both parties: The lender does not distinguish between primary applicant and co-borrower for repayment purposes. Both are equally liable for the entire loan.

CIBIL damage affects both: Any late payment, default, or settlement is reported on both credit reports simultaneously. This can prevent the co-borrower from accessing credit for their own needs for months or years.

Relationship risk: Joint financial obligations create legal and relational complications if the relationship between borrowers changes — divorce, family disputes, or business partnerships that dissolve.

FOIR impact on co-borrower: The joint loan EMI appears in the co-borrower’s obligations, which reduces their eligibility for future credit in their own name.

When a Joint Personal Loan Is the Right Choice

- Married couples with combined stable incomes who want a higher loan amount than either qualifies for individually

- Primary applicant with borderline CIBIL score (660-690) who has a family member with a strong score (720+) willing to co-borrow

- Borrowers who are new to credit (thin file) and have a creditworthy co-borrower who can anchor the application

- Situations where the loan is genuinely shared — home improvement benefitting both parties, joint medical expense, or joint financial goal

When You Should NOT Apply for a Joint Personal Loan

- When the primary applicant has a very bad credit history — a co-borrower helps, but a deeply negative CIBIL history may not be overcome by the co-borrower’s profile alone

- When the co-borrower has their own plans to borrow for a major purpose within the next 12-24 months — the joint loan EMI reduces their FOIR and borrowing capacity

- When the relationship between the borrowers is uncertain or could change — divorce proceedings, business disputes, or strained family relationships

- When only one party will benefit from the loan but both parties bear the legal risk

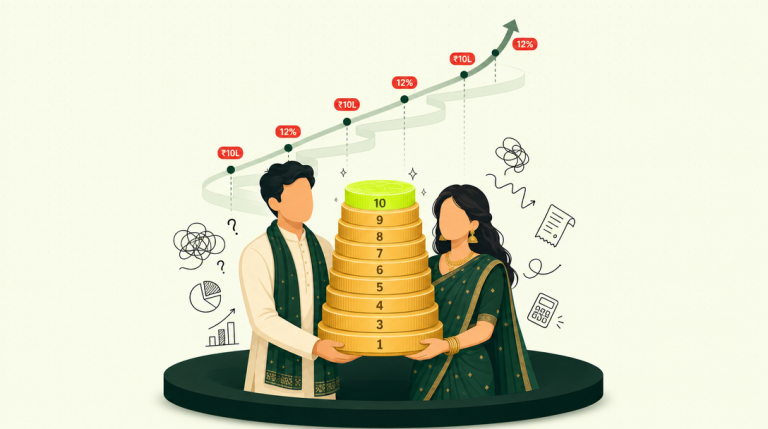

Joint Loan Eligibility: How Combined Income Is Calculated

Lenders combine the monthly take-home salaries of both applicants and calculate the maximum EMI they can service based on a maximum FOIR of 50-55%. Example: Primary applicant income Rs. 45,000/month. Co-borrower income Rs. 35,000/month. Combined income Rs. 80,000/month. Maximum EMI at 50% FOIR: Rs. 40,000/month. Existing EMIs both: Rs. 12,000/month. Available EMI capacity: Rs. 28,000/month. At 13% p.a. over 36 months, this supports a loan of approximately Rs. 8-9 lakh.

Understanding your FOIR before applying jointly is essential — both borrowers’ existing obligations are factored in. See: taptaploans.in/blog/foir-personal-loan-india/

Impact on Both Borrowers’ CIBIL Scores

A joint personal loan appears on both CIBIL reports from the date of approval. On-time payment improves both scores; late payment or default damages both scores simultaneously. The loan appears in both FOIR calculations for any future lending. Before applying jointly, both borrowers should check their individual CIBIL scores. See: taptaploans.in/blog/cibil-score-for-personal-loan-india/

How TapTap Loans Helps

TapTap Loans can assess both borrowers’ combined financial profile and identify whether a joint application meaningfully improves eligibility versus individual application, which lenders are likely to approve the joint profile and at what rate, and whether there are better alternatives for either borrower given their individual credit situations.

Key Takeaways

- Joint personal loans combine both applicants’ incomes, increasing the eligible loan amount significantly

- Both borrowers are 100% equally liable for the full loan — there is no proportional split of responsibility

- Any late payment or default damages both applicants’ CIBIL scores simultaneously

- The joint loan EMI reduces the co-borrower’s FOIR, limiting their future borrowing capacity

- Joint applications work best when both borrowers have stable income and a clear shared purpose for the loan

Frequently Asked Questions

A: Spouses are the most commonly accepted co-borrowers. Some lenders also accept parents, adult children, and siblings. The co-borrower must have verifiable income and ideally a good CIBIL score. Acceptance policies vary by lender.

A: Yes. A joint personal loan is reported on both applicants’ credit reports. On-time repayment builds the co-borrower’s credit history. Late payments or defaults damage both scores equally and simultaneously.

A: Removing a co-borrower from an active personal loan is generally not possible without refinancing the loan. You would need to foreclose the joint loan and take a new personal loan in your name alone — which requires you to qualify independently.

A: For borrowers who need a higher loan amount or have a borderline CIBIL score, a joint loan is beneficial. For borrowers who qualify individually at competitive rates, a joint loan adds the co-borrower to a liability without corresponding benefit.

A: If one borrower defaults, the lender has the right to pursue the other borrower for the full outstanding amount. Both CIBIL scores are impacted equally. There is no legal protection for the non-defaulting co-borrower from the lender’s perspective.

Conclusion

Joint personal loans are a powerful tool when used in the right circumstances — a legitimate way to access higher loan amounts and better terms through combined creditworthiness. But they require that both parties understand and accept full, equal liability for repayment. TapTap Loans can assess whether a joint application is the right move for your specific profile or whether alternatives serve you better.

| Ready to take the next step? TapTap Loans provides personalised loan advisory with no hard enquiries and no pressure. Visit taptaploans.in today. |